Greek project finance on the mend

Since the country's financial meltdown, project finance lending in Greece has slowly made a comeback in tandem with DFI support for a growing renewable energy and PPP project pipeline. Local banks have provided the vast majority of commercial debt and international lender participation is still very limited – but will that lending landscape change as more projects come to market?

Greece has seen an uptick in its project finance deal flow since its emergence from the depths of financial crisis a few years ago. Deals such as the recent €60 million project financing of National Energy’s solar PV portfolio demonstrate solid local commercial bank support for Greece’s expanding renewables sector. IFIs also continue to lend to Greece across a number of sectors, but the Greek project finance market remains largely untouched by international banks outside the oil and gas space.

According to Apostolos Gkoutzinis, a partner at Milbank: “Anything that forms part of the transition away from carbon-intensive fuels such as lignite, which has until recently been Greece’s predominant source of energy, into cleaner forms of energy is now the dominant project finance area. Greece is catching up with the rest of Europe in connection with energy transition, and there has been a lot of renewed enthusiasm and momentum in this area, especially since 2019 with the election of the present administration. Beyond renewables, other areas of significant project finance activity include infrastructure assets such as airports, motorways, ports, and logistics facilities. Other growing sectors include mining and telecommunications.”

Renewable energy transactions have quite clearly come to represent a significant proportion of project financings in Greece. The National Energy financing, which closed in late December 2021, is an indicator of commercial bank confidence in the bankability of renewables projects. The non-recourse bond loan facility will finance the construction of a 60MW portfolio of seven solar PV projects in Greece, including associated grid infrastructure. The projects are owned by National Energy's Greek subsidiary, New NE Solar Developments Two 2 Single Member SA (NNESD2), and include 51MW in the prefecture of Viotia, as well as 8.8MW in Peloponnese. Construction is underway and the projects are expected to be operational within H2 2022.

National Energy has been an active player in the Greek renewables sector, completing construction on a 24MWp portfolio of five projects in the regions of Viotia and Fthiotida in August 2021. The portfolio is backed by a €22 million non-recourse bond loan from Piraeus Bank. An additional recent solar transaction is the €8.7 million financing of PPC Renewables’ 15MW solar park in Ptolemaida, which was provided by National Bank of Greece and Eurobank.

In the institutional debt markets, GEK Terna raised €300 million in a sustainability-linked bond issuance in December. Piraeus Bank, Alpha Bank, Eurobank, and National Bank of Greece were joint coordinators and bookrunners on the financing. Bonds were priced at 2.30% and have a maturity of seven years. The EBRD took a €25 million ticket in the financing. The proceeds of the issuance will be used to refinance existing and future debts, to finance working capital needs, and to finance GEK Terna’s activities in the infrastructure, energy, industrial, and real estate sectors.

International commercial banks still largely absent

A consistent feature of the renewables sector and the broader project finance market in Greece is the primacy of local commercial banks and IFIs. The participation of international commercial lenders in Greek project finance has been very limited since the crisis. The €3.9 billion financing of the Trans Adriatic Pipeline is one exception, attracting a vast consortium of lenders, including Bank of China, BNP Paribas, MUFG, Caixa, Helaba, UBI Banca, Credit Agricole, Societe Generale, ING, Intesa Sanpaolo, Korea Development Bank, Mizuho, Natixis, Sabadell, Siemens Bank, Standard Chartered, SMBC, and UniCredit. It is also important to remember that this lending took place with immense DFI/ECA support from the EIB, the EBRD, Euler Hermes, SACE, and Bpifrance.

Such involvement from international lenders has not been mirrored in more recent transactions in the power or oil and gas sectors. In 2021, it was announced that the EIB and Eurobank had provided the €600 million financing of the Ariadne Interconnection, with the EIB also backing the €28.9 million financing of the North Macedonia gas interconnector project in 2022. The trend also applies to landmark infrastructure transactions such as the thirty-year €580 million financing of Athens Metro New Line 4 in 2022, which was provided by the EIB, as well as the €665.6 million deal for the twenty-year extension of the Athens Airport concession in 2019, which was underwritten by MLAs National Bank of Greece and Piraeus Bank.

There are several reasons for the limited participation of international banks in the Greek energy, infrastructure, and project finance markets. Discussing this point, Virginia Murray, a partner at Watson Farley & Williams, notes: “If we go back historically, international commercial banks were active in Greece. They all left during the financial crisis in Greece. As far as energy is concerned, they haven’t really come back, I think principally because the Greek banks are more competitive and more experienced in the field. They are able to move more quickly and they are very keen for the work. I think we might see some club deals with local and international lenders in the future as international lenders try to get back into the Greek market.”

As Murray points out, Greek banks are likely to be more competitive as a result of their knowledge of the local market, including its laws and permitting procedures. For example, the way in which project financings are typically structured in Greece differs markedly from international norms due to certain peculiarities in Greek law. Almost all large-scale commercial bank financings take the form of bond loan facilities, as there are substantial tax benefits in doing so.

Some of these benefits include avoiding making a contribution to the Bank of Greece, as would have to take place with a loan. Additionally, when security is registered with the public registry under a bond structure, a flat fee of €100 is payable, whereas this fee is calculated on the basis of the size of the loan if the transaction is structured as such. The loan structures with which international lenders are more familiar are, therefore, likely to be far more expensive than the bond loan format that is fairly unique to Greece.

The use of bond loan facilities in Greece is certainly not the sole driver behind the lack of international commercial bank participation. It is true that such lenders would have to become comfortable with typical Greek financing structures in order to avoid costly additional fees, but these structures do bear a fairly clear resemblance to more traditional project finance loans. Discussing the structure of bond loan facilities, Marisetta Marcopoulou, also a partner at Watson Farley & Williams, says: “Security is held by the bondholder agent, which is very close to the structure you would have for a loan governed by English law, as it is similar to the way a security trustee holds security in favour of the lenders. Because Greek law does not recognise the concept of a trust, if you do not have this type of structure with a bond loan, in syndicated loans, the security would need to be granted in favour of all lenders.”

Proceeding with a standard project finance loan in Greece would, therefore, bring complexities regarding security interests. Nevertheless, as Marcopoulou notes, bond loans are, ultimately, similar to syndicated loans where security interests are concerned and would not be completely foreign to international lenders if they simply pivoted to this structure instead of a syndicated loan. A further parallel is that the bondholder agent ensures that the bonds are freely transferrable, meaning that other lenders can join the transaction without complications relating to security interests, as would occur with a syndicated loan.

While the bond loan structure constitutes a barrier to international lenders, it is not so wholly different from conventional project finance lending as to be insurmountable. More probable causes of reticence towards Greece relate to deal flow, deal size, and lingering economic risks. Deal flow in Greece has certainly increased, but not to the extent that there are sufficient deals of sufficient size to allow international lenders to compete.

Renewables projects tend to fall below the utility-scale size benchmarks that draw in large consortiums of lenders. The deals that finance such projects are small enough not to interest international lenders and are readily backed by local banks, who have contacts with local developers and ample liquidity. This liquidity is boosted by a €2.7 billion guarantee from the EIB under the European Guarantee Fund to National Bank of Greece, Piraeus Bank, Alpha Bank, and Eurobank launched in February 2022.

Infrastructure projects in areas such as transport tend to be larger, but these projects are often supported by inexpensive IFI debt and have not occurred in great enough numbers to exceed the liquidity of the local banks that take parts with IFIs. There is also a great deal of motivation for local lenders to be seen to participate in large-scale infrastructure projects. As one industry expert puts it: “If a Greek lender cannot win the mandate to finance Athens Airport, what on Earth are they going to finance?”

Some economic uncertainty also still pervades the Greek market, although this has demonstrably improved in recent years. Fitch assigned Greece a rating of BB in January 2022, which is still below investment-grade. It is perhaps this context that is partially responsible for some risk-averse lending practices. Roman Matkiwsky, director in energy and infrastructure at BSTDB, says: “What we are finding is a lot of the Greek renewables projects have been financed on a corporate basis by the commercial banks here in Greece. What we find is that debt will be raised on the basis of the company and then after the project becomes operational they convert it to project finance debt.” The requirement to mitigate construction risk with corporate debt is an indicator of a continued hesitance from lenders, even in the sector with the greatest deal flow. This hesitance will need to abate if international banks are to make a re-entry into Greek project finance lending.

The Uxolo perspective

Greece still has a long way to go in terms of producing solid project finance deal flow. Nevertheless, there are definite signs of robust expansion, even in the aftermath of the Covid-19 pandemic which caused the Greek economy to contract by 9% in 2020. Projections for 2022 are more positive, with the European Commission forecasting GDP growth of 4.9% year-on-year. The Greek government is also putting in place further renewable energy tenders and a pipeline of PPP projects.

In late 2021, the European Commission approved Greece’s application for a €2.27 billion state-aid scheme to support the development of 4.2GW of energy generation capacity across multiple sectors. According to the European Commission these sectors include ‘onshore wind, photovoltaic, wind and photovoltaic with storage, biogas, biomass, landfill gas, hydroelectric power, concentrated solar power and geothermal power plants’. The support will largely be offered through a contracts for difference (CfD) regime for a period of twenty years and must be taken up by 2025. The programme is expected to be codified in legislation soon, after which energy auctions will begin to take place.

In terms of PPP project development, the Greek government formally mandated the EBRD to devise a series of PPP projects and tenders under a €20 million programme in 2020. The EBRD works with the government to prepare the projects and supervises project development. Sources confirm that the tender for a biomedical facility in Athens is at an advanced stage and is nearing commercial close. The EBRD also has several other PPP projects under development, including the Minagiotiko Dam and Tavropos Irrigation Networks irrigation projects; student accommodation for the University of Thessaly; a comprehensive e-mobility strategy that will result in a number of different projects; and an urban regeneration project to convert a former factory site into a park and a complex of buildings that will house nine government ministries.

The University of Thessaly project will move to tender fairly shortly and has completed designs, feasibility studies, and permits. Greece has also developed and continues to develop PPPs outside of the EBRD mandate. Two existing concessions that will come up for renewal soon – also inviting project finance debt – are the Egnatia and Attiki Odos motorway concessions.

Referencing Greek PPP development, Maria Tzanidaki, principle manager, PPP advisory unit at the EBRD, says: “The PPP unit in Greece has been very active in structuring PPPs in various sectors, such as waste management, water resources, roads, and highways. They have a pipeline of around 42-45 PPPs. The EBRD supports the government in structuring 10-11 PPPs. The two irrigation projects on which the EBRD is working have the challenge of being financed with blended finance from the RRF [EU Recovery and Resilience Fund] and Greece has not seen blending with RRF before. There are time restrictions on the use of the RRF that need to be managed within the partnership agreement.”

With tangible progress being made on a programme of both renewable energy and PPP projects, Greek project finance deal flows stand to increase further in 2022 and beyond. As the volume of larger deals increases, space may be created for international lenders in club deals with experienced Greek banks, particularly if Greece receives an investment-grade credit rating. For the time being, however, the Greek project finance market will still be dominated by local banks and IFIs.

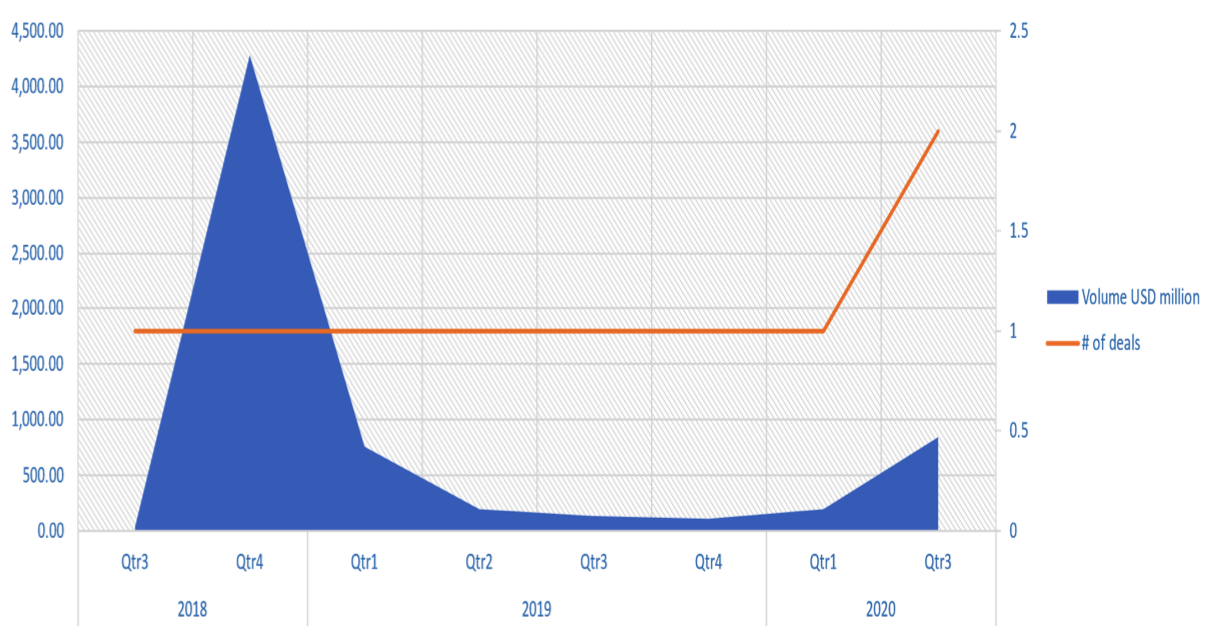

The size of the Greek project finance market between 2018 and 2020, according to Proximo Data. The sharp spike in 2018 is a result of the Trans Adriatic Pipeline financing.